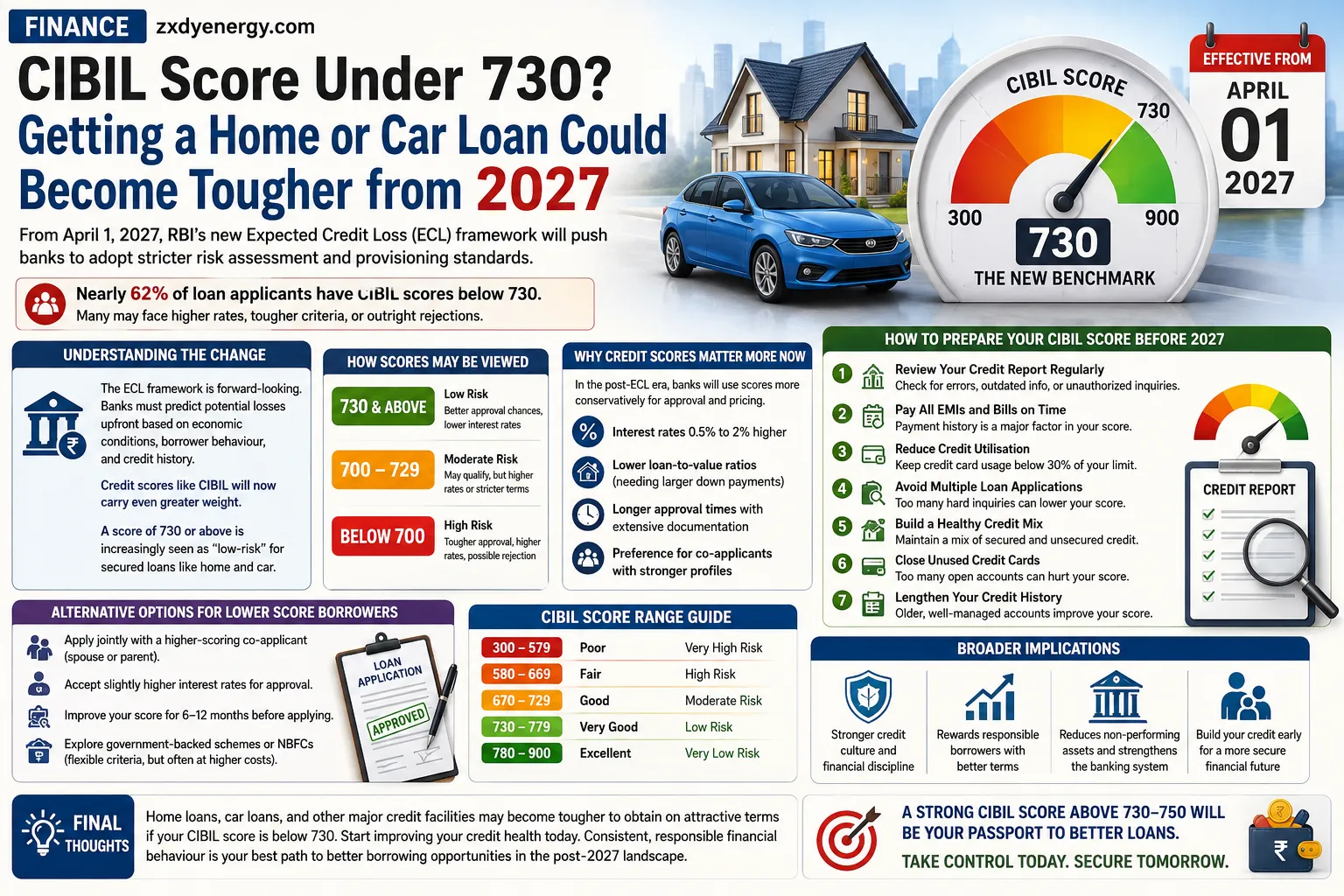

For millions of Indians, purchasing a home or upgrading to a new car represents one of life’s most significant financial milestones. These loans often mark important milestones — from starting a family to achieving long-term security. However, starting in 2027, securing such credit may become noticeably more challenging for those with a CIBIL score below 730. This shift stems from the Reserve Bank of India’s (RBI) upcoming Expected Credit Loss (ECL) framework, set to take effect from April 1, 2027, which will compel banks to adopt far stricter risk assessment and provisioning standards.

This change could impact a substantial portion of borrowers. Industry estimates suggest that nearly 62% of loan applicants currently have CIBIL scores below 730, meaning a large segment of the population may face higher interest rates, stricter eligibility criteria, additional collateral requirements, or even outright rejections for major loans.

Understanding the Upcoming Changes

The ECL framework represents a fundamental shift in how banks evaluate and provision for credit risk. Under the previous incurred loss model, banks set aside provisions only after loans turned bad. The new forward-looking ECL approach requires banks to predict potential losses upfront based on sophisticated models that factor in economic conditions, borrower behaviour, and credit history.

In this heightened risk environment, credit scores like CIBIL will carry even greater weight. While the RBI has not mandated a strict minimum score cutoff, banks are expected to tighten internal lending policies. A score of 730 or above is increasingly viewed as a benchmark for “low-risk” borrowers for secured loans like home and car financing. Scores in the 700–729 range may still qualify but could attract higher interest rates or more rigorous scrutiny. Those below 700 are likely to face the toughest challenges.

Why Credit Scores Matter More Now

CIBIL scores, ranging from 300 to 900, summarize an individual’s credit behaviour based on repayment history, credit utilisation, length of credit history, and types of credit used. A higher score signals reliability to lenders.

In the post-ECL era, banks will use these scores more conservatively to determine not just approval but also pricing. Borrowers with scores above 750–780 typically enjoy the best rates and terms. Those below 730 may see:

- Interest rates 0.5% to 2% higher.

- Lower loan-to-value ratios (requiring larger down payments).

- Longer approval times with extensive documentation.

- Preference for co-applicants with stronger profiles.

This evolution aligns with global best practices and aims to strengthen the banking system’s resilience against potential economic downturns.

How to Prepare Your CIBIL Score Before 2027

With the deadline approaching, proactive steps can significantly improve your chances of securing favourable loan terms:

1. Review Your Credit Report Regularly

Obtain your free annual CIBIL report and check for errors, outdated information, or unauthorised inquiries. Dispute inaccuracies promptly, as corrections can boost your score within weeks.

2. Pay All EMIs and Bills on Time

Payment history accounts for a substantial portion of your score. Even occasional delays can cause sharp drops. Set up auto-debit mandates or calendar reminders to maintain consistency.

3. Reduce Credit Utilisation

Keep your credit card utilisation below 30% of the limit. High utilisation signals financial stress to lenders.

4. Avoid Multiple Loan Applications

Frequent hard inquiries can temporarily lower your score. Space out applications and focus on pre-approvals where possible.

5. Build a Healthy Credit Mix

A balanced mix of secured (home/car) and unsecured (credit cards) credit, managed responsibly, demonstrates financial maturity.

6. Close Unused Credit Cards

Too many open accounts can negatively impact your score. Close dormant ones strategically.

7. Lengthen Your Credit History

Older, well-managed accounts positively influence your score. Avoid closing long-standing accounts unless necessary.

Alternative Options for Lower Score Borrowers

Even with a moderate score, borrowing remains possible. Consider:

- Joint applications with a higher-scoring co-applicant (spouse or parent).

- Opting for slightly higher interest rates in exchange for approval.

- Improving your score for 6–12 months before applying.

- Exploring government-backed schemes or NBFCs that may have more flexible criteria (though often at higher costs).

Broader Implications for Indian Borrowers

This policy shift encourages greater financial discipline across the population. It rewards responsible borrowers while pushing others toward better credit habits. In the long run, a stronger credit culture benefits the entire economy by reducing non-performing assets and enabling more stable lending.

For young professionals and first-time borrowers, building a solid credit history early becomes even more critical. Parents should also consider guiding their children toward responsible credit use from an early age.

Final Thoughts

The RBI’s ECL framework, effective from 2027, marks a significant tightening of lending standards aimed at creating a more robust banking sector. For individuals with CIBIL scores below 730, home loans, car loans, and other major credit facilities may indeed become tougher to obtain on attractive terms.

The message is clear: start improving your credit health today. Consistent, responsible financial behaviour is the most reliable path to maintaining access to credit in this evolving landscape. Whether you are planning to buy a home in the next few years or simply want financial flexibility, a strong CIBIL score above 730–750 will increasingly serve as your passport to better borrowing opportunities.

Take control of your credit profile now. Review your report, adopt disciplined repayment habits, and position yourself favourably before the 2027 changes fully take effect. Your future self — and your family’s financial dreams — will thank you for it.