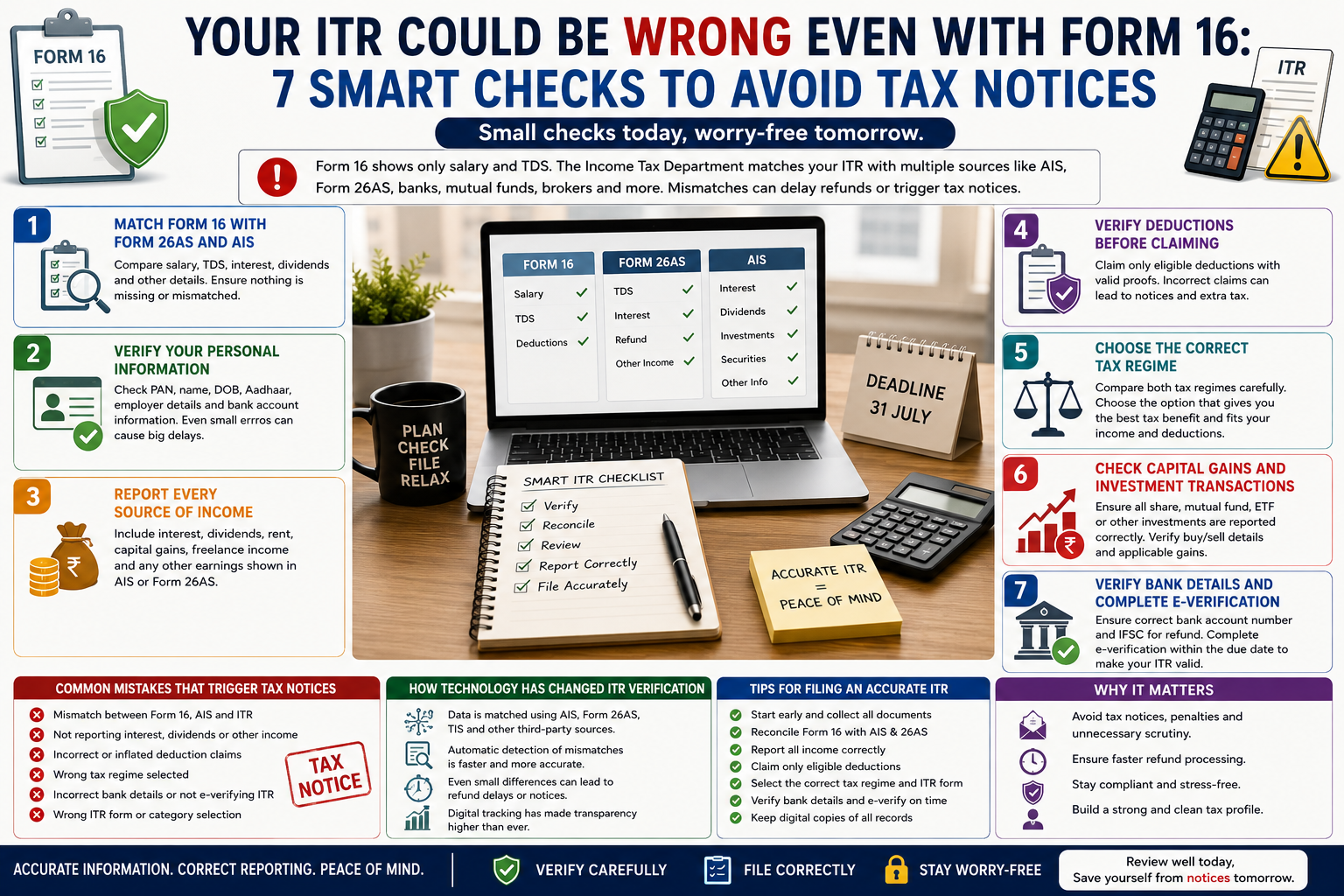

For most salaried employees, Form 16 is the primary document used while filing an Income Tax Return (ITR). Since it contains salary details, tax deducted at source (TDS), and deductions reported by the employer, many taxpayers assume that simply uploading Form 16 is enough to file an accurate return.

For most salaried employees, Form 16 is the primary document used while filing an Income Tax Return (ITR). Since it contains salary details, tax deducted at source (TDS), and deductions reported by the employer, many taxpayers assume that simply uploading Form 16 is enough to file an accurate return.

However, with the Income Tax Department now using advanced digital verification systems, relying only on Form 16 may lead to errors. Information from the Annual Information Statement (AIS), Form 26AS, Taxpayer Information Summary (TIS), banks, mutual funds, stock brokers, and other reporting entities is automatically matched with your ITR. Even a small mismatch can delay your refund or trigger a tax notice.

Before submitting your return, it is important to verify all tax-related information carefully. Here are seven smart checks that can help you file an accurate ITR and avoid unnecessary tax issues.

Why Form 16 Alone Is Not Enough

Form 16 is issued by your employer and mainly covers salary income and TDS deducted on that salary. However, it does not necessarily include every source of income you earned during the financial year.

For example, interest earned from savings accounts or fixed deposits, dividend income, capital gains from shares or mutual funds, rental income, or income from freelance work may not appear in Form 16. These transactions are often reported separately in AIS or Form 26AS.

Since the Income Tax Department compares multiple data sources, taxpayers should treat Form 16 as the starting point of tax filing rather than the final document.

1. Match Form 16 With Form 26AS and AIS

The first and most important step is comparing your Form 16 with Form 26AS and the Annual Information Statement.

Form 26AS shows taxes deducted and deposited against your PAN, while AIS contains a wider range of financial information, including interest income, dividends, securities transactions, mutual fund investments, and other reported financial activities.

If any income or TDS reflected in these documents is missing from your return, it may result in refund delays or scrutiny. Carefully reconciling these documents before filing significantly reduces the chances of receiving a tax notice.

2. Verify Your Personal Information

Small mistakes in personal details can create unnecessary complications during processing.

Check that your PAN, name, date of birth, Aadhaar details, employer information, and bank account numbers are correct in your Form 16 and ITR.

Incorrect personal information may delay refund processing or create verification issues later. Verifying these details only takes a few minutes but can prevent avoidable problems.

3. Report Every Source of Income

Many taxpayers unintentionally omit income because they assume only salary needs to be reported.

Income earned through bank interest, fixed deposits, dividends, rental property, capital gains, freelance work, or other investments may also be taxable depending on the applicable provisions.

AIS often reflects these transactions because they are reported by banks, financial institutions, brokers, or other entities.

Failing to disclose these income sources may create mismatches that are automatically detected during return processing.

4. Verify Deductions Before Claiming Them

Tax deductions should always be supported by valid records and should match applicable tax rules.

Before claiming deductions under eligible sections, verify that they are correctly reflected in Form 16 where applicable or supported by proper documentation.

Incorrect deduction claims may reduce tax liability temporarily, but they can also result in notices if the claims cannot be substantiated during verification.

Maintaining proper records helps support genuine claims if clarification is required in the future.

5. Choose the Correct Tax Regime

Selecting the correct tax regime has become an important part of filing an accurate ITR.

Depending on your eligibility, deductions, exemptions, and income structure, one regime may be more beneficial than the other.

Many taxpayers mistakenly select the wrong option without comparing both tax regimes, resulting in higher tax liability or filing errors.

Review your salary structure, deductions, and overall tax calculations carefully before making your selection.

6. Check Capital Gains and Investment Transactions

If you invested in shares, mutual funds, exchange-traded funds, or other securities during the financial year, ensure that all taxable transactions are reported correctly.

Many investment-related transactions appear in AIS even if they are not included in Form 16.

Capital gains calculations should be prepared using accurate purchase prices, sale values, holding periods, and applicable tax rules.

Ignoring investment transactions is one of the common reasons for discrepancies during return processing.

7. Verify Bank Details and Complete E-Verification

Even after successfully submitting an ITR, one important step still remains—e-verification.

An Income Tax Return is considered incomplete until it is verified within the prescribed time limit.

Taxpayers should also ensure that their bank account details are accurate because incorrect account information may delay refunds.

Completing e-verification and confirming bank details ensures faster processing and reduces unnecessary complications.

Common Mistakes That Can Trigger Tax Notices

Several avoidable mistakes increase the likelihood of receiving notices from the Income Tax Department.

These include reporting incorrect salary figures, failing to disclose interest income, missing capital gains, claiming unsupported deductions, selecting the wrong ITR form, entering incorrect bank details, or forgetting to e-verify the return.

Since tax systems now automatically compare information reported by employers, banks, financial institutions, and brokers, inconsistencies are much easier to detect than before.

How Technology Has Changed ITR Verification

The Income Tax Department has significantly improved its digital verification systems.

Financial information from multiple reporting entities is now consolidated through platforms such as AIS, Form 26AS, and TIS. This allows authorities to compare taxpayer disclosures with independently reported information.

As a result, manual errors, omitted income, or mismatched tax credits are identified much faster than in previous years.

This makes careful review before filing more important than ever.

Tips for Filing an Accurate ITR

The safest approach is to begin tax preparation early instead of waiting until the deadline.

Review Form 16 carefully, compare it with AIS and Form 26AS, verify every income source, confirm deduction claims, select the correct tax regime, and ensure that your bank details are correct before submission.

Finally, complete e-verification immediately after filing and retain digital copies of important tax documents for future reference if any clarification is required.

Frequently Asked Questions (FAQs)

Is Form 16 enough to file an Income Tax Return?

No. Form 16 mainly covers salary income and TDS. Taxpayers should also review Form 26AS, AIS, and other financial records before filing.

Why should I check AIS before filing my ITR?

AIS contains details of various financial transactions, including interest income, dividends, investments, and securities transactions. Matching it with your ITR helps avoid mismatches.

Can incorrect information delay my tax refund?

Yes. Incorrect bank details, mismatched TDS, missing income disclosures, or failure to e-verify the return can delay refund processing or lead to notices.

Conclusion

Form 16 remains one of the most important documents for salaried taxpayers, but it should never be considered the only document required for filing an accurate Income Tax Return. With the Income Tax Department using advanced data matching through AIS, Form 26AS, TIS, and other financial reporting systems, even minor mistakes can result in refund delays or tax notices.

By carefully matching your records, reporting every source of income, verifying deductions, selecting the correct tax regime, reviewing investment transactions, and completing e-verification, you can significantly reduce the risk of filing errors.

A few extra minutes spent reviewing your tax information today can save you from unnecessary notices, additional tax demands, and lengthy correction procedures later.