Taking a loan together with a spouse, family member, or partner may seem like a practical financial decision. Joint loans can increase borrowing capacity, improve chances of approval, and help people achieve major goals such as buying a home, funding education, or managing large expenses.

However, joint borrowing also comes with responsibilities that many people do not fully understand. A joint loan is not just a shared financial benefit; it is also a shared legal obligation. If one borrower fails to repay the loan, the other borrower can still be held responsible for the entire outstanding amount.

Real-life situations involving separation, relationship conflicts, or financial disagreements show how joint loans can create unexpected problems. In many cases, a person who did not spend the money or cause the default may still face difficulties while applying for future loans because their credit history is connected to the loan.

Understanding how joint loans work and knowing the risks before signing an agreement can help individuals protect their financial future.

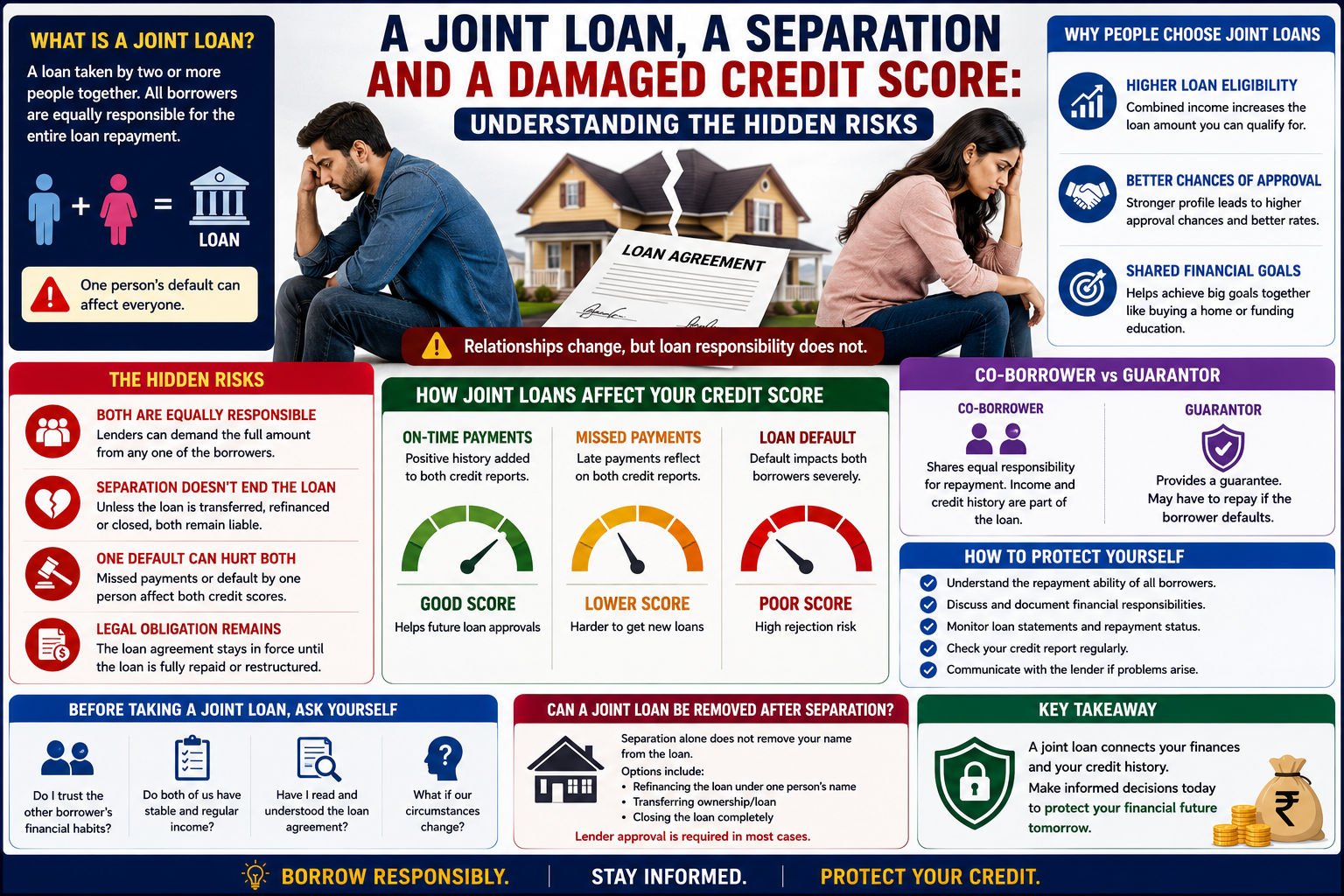

What Is a Joint Loan?

A joint loan is a financial agreement where two or more individuals apply for and become responsible for the same loan. All borrowers are considered equally responsible for repayment, regardless of who actually uses the borrowed money.

For example, a married couple may apply for a home loan together. Both names appear on the loan agreement, and both borrowers are responsible for making timely repayments.

Similarly, parents and children may take joint education loans, or business partners may apply for joint financing.

The important point is that lenders do not usually divide responsibility based on who benefited more from the loan. Every borrower is responsible for ensuring that the repayment obligations are fulfilled.

Why People Choose Joint Loans

Many individuals choose joint loans because they offer several financial advantages.

Higher Loan Eligibility

When two people combine their incomes, lenders may consider a higher repayment capacity. This can increase the amount of loan available compared to applying individually.

For example, a couple applying for a home loan may qualify for a larger amount because both incomes are considered.

Better Chances of Approval

A joint applicant with a stable income or strong credit history can improve the overall loan application profile.

This can be helpful for borrowers who may not qualify for a loan independently.

Shared Financial Goals

Joint loans are often used by couples and family members who want to achieve common financial goals, such as purchasing property or funding important expenses.

However, these benefits come with shared responsibilities that should not be ignored.

The Hidden Risk: Both Borrowers Are Responsible for Repayment

One of the biggest misunderstandings about joint loans is that each person is responsible only for their portion of the repayment.

In reality, lenders usually consider all borrowers equally responsible for the complete loan amount.

If one borrower stops paying, the lender can demand repayment from the other borrower.

For example, if a couple takes a home loan together and later separates, the loan responsibility does not automatically disappear. Even if one person moves out or stops contributing, the lender can still expect repayment from either borrower.

This creates a situation where personal relationships and financial obligations become closely connected.

How Separation Can Create Financial Problems

Relationship separation can make joint loans more complicated.

Many people assume that after separation, each person’s financial responsibilities automatically become separate. However, a loan agreement does not change simply because a relationship ends.

Unless the loan is officially restructured, transferred, or fully repaid, both borrowers remain responsible.

For example, if one partner continues living in a jointly financed house but stops making payments, the other partner may still face consequences if repayments are missed.

Missed payments can affect both borrowers’ credit records, even if only one person failed to contribute.

How Joint Loans Affect Credit Scores

A credit score reflects a person’s history of managing borrowed money. Timely payments can help maintain a healthy credit profile, while missed payments, defaults, and high debt levels can negatively affect the score.

In a joint loan, repayment behavior is usually linked to all borrowers.

This means:

If payments are made on time, both borrowers may benefit from a positive repayment history.

If payments are missed, both borrowers may experience negative effects.

If the loan goes into default, both borrowers’ credit profiles may be affected.

This is why agreeing to become a co-borrower requires careful consideration.

When Someone Else’s Loan Can Become Your Problem

Many people agree to joint loans because they trust their spouse, family member, or friend. However, financial situations can change unexpectedly.

A person may lose their job, experience business losses, face health expenses, or simply fail to manage repayments properly.

Even if the second borrower had no involvement in spending the loan amount, they may still face consequences.

For example, someone who became a joint borrower for a relative’s loan may later struggle to get a personal loan because the existing debt affects their credit profile.

Trust is important in relationships, but financial agreements require a clear understanding of legal responsibilities.

The Difference Between a Co-Borrower and a Guarantor

Many people confuse co-borrowers with guarantors, but their responsibilities can differ.

A co-borrower is directly responsible for repaying the loan along with the primary borrower. Their income, credit history, and repayment responsibility are usually considered part of the loan agreement.

A guarantor provides a guarantee that the loan will be repaid if the borrower fails to meet obligations. Depending on the agreement, the guarantor may also face repayment responsibility if the borrower defaults.

Both roles involve financial risk and should not be accepted without understanding the consequences.

Important Things to Consider Before Taking a Joint Loan

Before signing a joint loan agreement, individuals should carefully evaluate their decision.

Understanding the repayment ability of all borrowers is essential. A person should consider whether the other borrower has stable income, responsible financial habits, and a reliable repayment record.

Discussing financial responsibilities clearly can prevent future misunderstandings. Borrowers should decide who will contribute how much toward repayment and maintain proper records.

It is also important to understand the loan agreement, repayment terms, interest rates, and consequences of missed payments.

A joint loan should be treated as a serious long-term financial commitment.

How to Protect Yourself From Joint Loan Problems

Individuals can take several steps to reduce risks associated with joint borrowing.

Maintaining open communication about finances is important, especially among couples and family members.

Regularly checking loan statements and repayment status can help identify problems early.

Keeping personal credit records updated and monitoring credit reports can also help borrowers understand their financial position.

If circumstances change, borrowers should communicate with the lender about possible solutions instead of allowing missed payments to accumulate.

Ignoring repayment issues can create larger financial problems in the future.

Can a Joint Loan Be Removed After Separation?

Many people believe that separation automatically removes their name from a joint loan. However, this is usually not the case.

Removing a borrower’s name generally requires approval from the lender. Possible solutions may include refinancing the loan under one person’s name, transferring ownership arrangements, or closing the loan completely.

Until the lender officially changes the agreement, both borrowers remain responsible.

This is why financial planning during separation is extremely important.

Conclusion

Joint loans can be useful financial tools, but they also carry significant responsibilities. A person who agrees to share a loan is also agreeing to share the repayment risk.

Cases where one person suffers credit damage despite not using the money highlight an important lesson: financial commitments should never be accepted without complete understanding.

Whether the loan is taken with a spouse, family member, or friend, borrowers should carefully evaluate trust, repayment ability, and long-term consequences.

A joint loan connects not only finances but also credit histories. Making an informed decision before signing can help protect financial stability and prevent unexpected problems in the future.